The global financial system is undergoing one of the most significant transformations in modern history. While cryptocurrencies such as Bitcoin and Ethereum introduced the concept of digital money to the public, governments and central banks have been developing their own version of digital currency known as Central Bank Digital Currencies (CBDCs).

In 2026, CBDCs have moved beyond theoretical discussions and research papers. Many countries have launched pilot programs, conducted real-world testing, and expanded digital currency initiatives. Some nations have already introduced operational CBDCs, while others continue evaluating potential benefits and risks.

As digital payments become increasingly dominant, central banks are exploring how CBDCs can improve financial systems, support economic growth, enhance payment efficiency, and maintain monetary sovereignty in a rapidly changing world.

This article examines the latest CBDC developments, their benefits and challenges, and what they could mean for consumers, businesses, financial institutions, and governments.

What Is a CBDC?

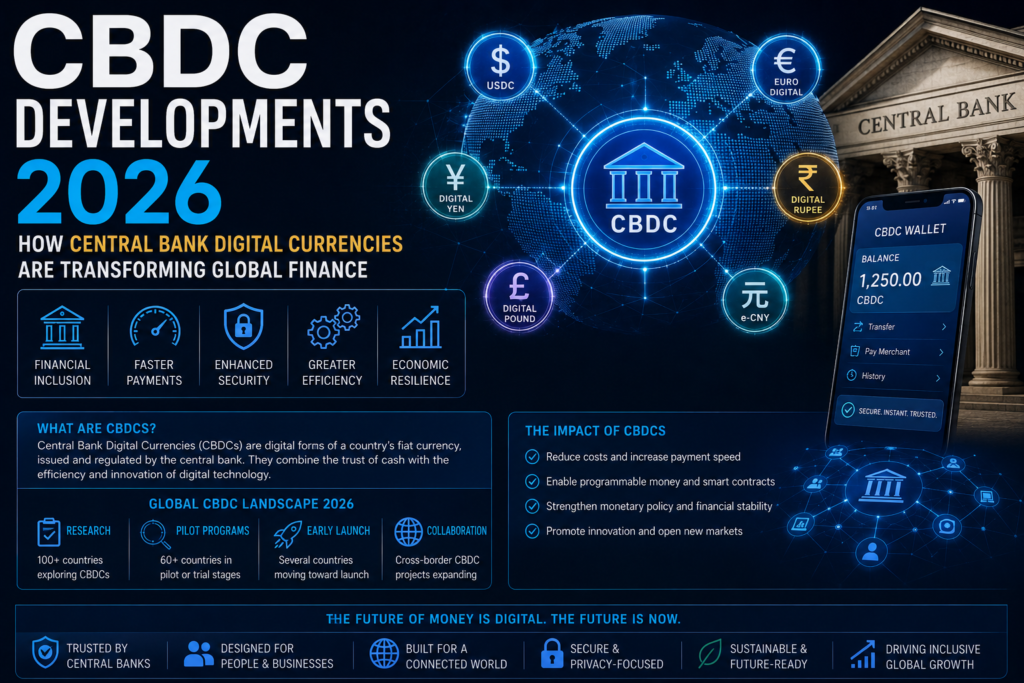

A Central Bank Digital Currency (CBDC) is a digital form of a country’s official currency issued and backed by its central bank.

Unlike cryptocurrencies, CBDCs are not decentralized. They are government-issued digital currencies that represent a direct claim on the central bank.

CBDCs are designed to combine the convenience of digital payments with the trust and stability of sovereign money.

Examples include:

- Digital versions of national currencies

- Retail CBDCs for public use

- Wholesale CBDCs for financial institutions

- Cross-border settlement systems

CBDCs are fundamentally different from cryptocurrencies because they are controlled by central authorities and maintain legal tender status.

Why Are Central Banks Exploring CBDCs?

Several factors are driving global interest in digital currencies.

Declining Cash Usage

Many countries are experiencing a significant reduction in cash transactions.

Consumers increasingly prefer:

- Mobile payments

- Digital wallets

- Online banking

- Contactless transactions

CBDCs provide central banks with a way to support modern payment preferences.

Growth of Private Digital Assets

The rapid expansion of cryptocurrencies and stablecoins has encouraged governments to explore alternatives that preserve monetary control.

Payment System Modernization

Many existing payment infrastructures were developed decades ago.

CBDCs can support:

- Faster transactions

- Lower costs

- Improved efficiency

- Greater accessibility

Financial Inclusion

Digital currencies may help provide financial services to underserved populations.

Types of CBDCs

CBDCs generally fall into two categories.

Retail CBDCs

Retail CBDCs are designed for use by individuals and businesses.

Potential use cases include:

- Everyday purchases

- Peer-to-peer transfers

- Digital savings

- Government benefit payments

Retail CBDCs function similarly to digital cash.

Wholesale CBDCs

Wholesale CBDCs are intended for financial institutions.

Applications include:

- Interbank settlements

- Securities transactions

- Cross-border payments

- Financial market infrastructure

Wholesale CBDCs often focus on improving efficiency within the banking system.

Global CBDC Developments in 2026

Countries around the world are advancing CBDC initiatives at different speeds.

Asia’s Leadership Role

Several Asian nations remain at the forefront of CBDC innovation.

Governments continue testing:

- Digital payment networks

- Cross-border settlement systems

- Wholesale financial applications

- Retail payment solutions

Asia’s strong digital infrastructure has supported rapid experimentation.

Europe’s Digital Currency Initiatives

European policymakers continue evaluating digital currency frameworks designed to complement existing payment systems.

Key priorities include:

- Privacy protections

- Financial stability

- Consumer convenience

- Regulatory compliance

North American Developments

Central banks in North America continue studying the potential implications of digital currencies.

Research focuses on:

- Economic impacts

- Financial inclusion

- Cybersecurity

- Monetary policy considerations

Key Benefits of CBDCs

Supporters argue that CBDCs offer numerous advantages.

Faster Payments

Traditional payment systems can involve delays, especially for international transfers.

CBDCs may enable:

- Real-time transactions

- Instant settlement

- Reduced processing times

Lower Transaction Costs

Digital infrastructure can potentially reduce payment processing expenses.

This may benefit:

- Consumers

- Businesses

- Governments

Improved Financial Inclusion

Millions of people worldwide remain unbanked or underbanked.

CBDCs could provide access to digital financial services without requiring traditional bank accounts.

Enhanced Payment Security

Government-backed digital currencies may offer secure payment alternatives supported by central bank infrastructure.

Reduced Dependence on Cash

Digital currencies provide a modern alternative as societies increasingly adopt electronic payments.

CBDCs and Financial Inclusion

Financial inclusion remains one of the strongest arguments for CBDC adoption.

Many individuals face barriers to accessing traditional financial services.

These barriers may include:

- Geographic limitations

- High banking fees

- Documentation requirements

- Lack of financial infrastructure

CBDCs could help address these challenges by providing accessible digital payment tools.

Potential Benefits

Users may gain access to:

- Digital savings options

- Secure payments

- Government assistance programs

- Financial services

This could support economic participation and financial empowerment.

Cross-Border Payments and CBDCs

International payments often remain slow, expensive, and complex.

Cross-border CBDC initiatives seek to improve this process.

Current Challenges

Traditional international transfers may involve:

- Multiple intermediaries

- High fees

- Delayed settlements

- Currency conversion complexities

CBDC Solutions

CBDCs may facilitate:

- Faster settlement

- Reduced costs

- Greater transparency

- Improved efficiency

Many central banks are actively exploring cross-border use cases.

CBDCs and Monetary Policy

Central banks use monetary policy to manage economic conditions.

CBDCs may introduce new tools and capabilities.

Potential Advantages

Digital currencies could provide:

- Better payment data

- Faster policy transmission

- Improved economic monitoring

Important Considerations

Policymakers must carefully balance innovation with economic stability.

Changes to monetary systems require extensive testing and evaluation.

Impact on Commercial Banks

One of the most debated topics surrounding CBDCs involves their impact on commercial banks.

Potential Opportunities

Banks could benefit from:

- Modernized infrastructure

- Improved settlement systems

- New service offerings

Potential Concerns

Some experts worry that consumers could move deposits from banks into CBDC accounts.

This could affect:

- Bank funding models

- Lending activities

- Financial stability

Central banks continue studying these implications carefully.

CBDCs vs Cryptocurrencies

CBDCs and cryptocurrencies are often compared, but they serve different purposes.

CBDCs

- Government-issued

- Centralized control

- Legal tender status

- Stable value

- Regulatory oversight

Cryptocurrencies

- Decentralized networks

- Market-driven valuation

- Variable prices

- Independent governance models

Both may coexist within future financial ecosystems.

CBDCs and Stablecoins

Stablecoins have become increasingly popular for payments and settlements.

Many observers view CBDCs and stablecoins as complementary technologies.

Similarities

Both aim to provide:

- Digital transactions

- Faster payments

- Reduced friction

Differences

CBDCs are issued by governments, while stablecoins are generally issued by private organizations.

Future payment systems may incorporate both solutions.

Privacy and Security Concerns

Privacy remains one of the most discussed aspects of CBDCs.

Citizens often express concerns regarding:

- Transaction monitoring

- Data collection

- Government oversight

Balancing Privacy and Compliance

Central banks seek to balance:

- User privacy

- Anti-money laundering requirements

- Financial crime prevention

Achieving this balance is essential for public trust.

Cybersecurity

Strong cybersecurity protections are necessary to defend digital currency systems from attacks and operational disruptions.

Technological Infrastructure Requirements

Launching a CBDC requires sophisticated technology infrastructure.

Key requirements include:

- Secure networks

- Digital wallets

- Identity verification systems

- Transaction processing capabilities

- Disaster recovery mechanisms

Scalability and reliability are critical factors for national payment systems.

Challenges Facing CBDC Adoption

Despite growing interest, several challenges remain.

Technical Complexity

Developing secure and scalable systems requires significant expertise and investment.

Regulatory Considerations

Governments must establish legal frameworks that support digital currency operations.

Public Trust

Adoption depends on consumer confidence and understanding.

Financial Stability Risks

Poorly designed systems could create unintended economic consequences.

Careful planning is necessary to address these challenges.

The Role of CBDCs in the Future Economy

CBDCs may play a significant role in future financial ecosystems.

Potential applications include:

- Digital commerce

- Government payments

- International settlements

- Financial inclusion programs

- Smart payment systems

As technology evolves, additional use cases are likely to emerge.

Future Trends in CBDC Development

Several trends are expected to shape the next phase of digital currency innovation.

Increased Pilot Programs

More countries will continue testing real-world implementations.

Cross-Border Collaboration

Central banks may cooperate on international settlement systems.

Integration With Existing Financial Systems

CBDCs will likely complement rather than replace current banking infrastructure.

Greater Consumer Awareness

Public understanding of digital currencies is expected to improve over time.

Expansion of Digital Payment Ecosystems

CBDCs may become part of broader digital finance strategies.

What Businesses Should Know

Organizations should monitor CBDC developments closely.

Potential business impacts include:

- Payment system modernization

- Faster settlements

- Reduced transaction costs

- New financial products

- Enhanced customer experiences

Early preparation may help businesses adapt more effectively.

Conclusion

CBDCs represent one of the most important financial innovations of the digital age.

As central banks around the world explore digital currencies, the global financial system is entering a new era characterized by greater digitization, improved payment efficiency, and evolving monetary infrastructure.

While significant challenges remain, CBDCs have the potential to enhance financial inclusion, modernize payments, and strengthen economic resilience.

The coming years will be critical in determining how digital currencies integrate into everyday life and how they coexist with traditional banking systems, cryptocurrencies, and private payment solutions.

For consumers, businesses, investors, and policymakers, understanding CBDC developments will be essential for navigating the future of money.